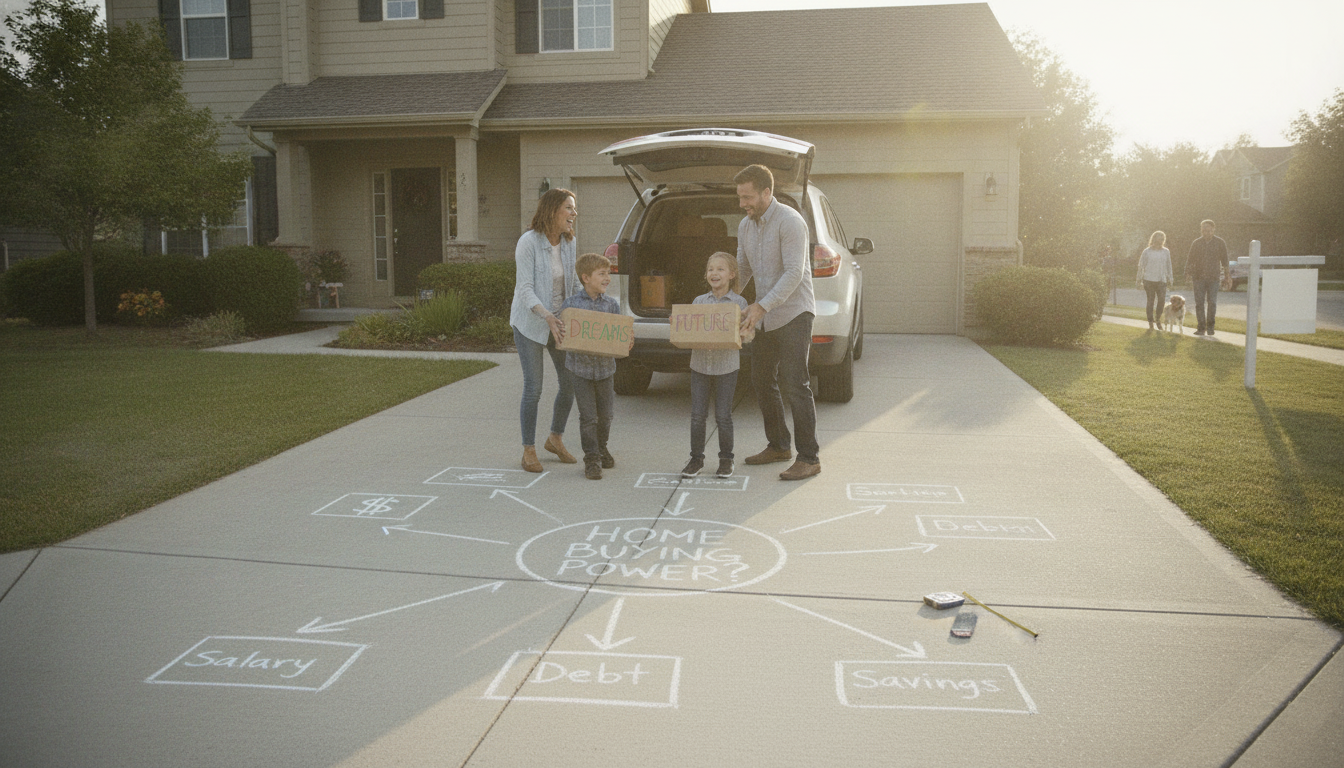

Income Multiplier Explained: Estimate Home Buying Power

What is an income multiplier?

An income multiplier is a number lenders and financial planners use to estimate how much home you may be able to afford based on your annual income. It’s a quick rule-of-thumb that turns income into an approximate price range by multiplying your gross yearly earnings by a set factor (often influenced by current lending standards, interest rates, and your overall financial profile).

How does an income multiplier work?

The idea is simple: start with your income, then apply a multiplier to get a rough affordability target. For example, if your household earns $90,000 per year and a lender uses a 4x multiplier, the estimate for a potential purchase price might be around $360,000. Some lenders may use a different multiplier depending on whether they’re evaluating a first-time buyer, a conventional loan, or a higher-debt scenario.

It’s important to treat this as an estimate—not a guarantee. A multiplier doesn’t automatically account for key details like property taxes, HOA dues, insurance, or how interest rates change your monthly payment.

What affects the income multiplier a lender may use?

Income multipliers aren’t one-size-fits-all. Common factors that can raise or lower the multiplier include:

- Debt-to-income (DTI) ratio: Higher monthly debt payments can reduce what you qualify for.

- Credit score and credit history: Strong credit often improves pricing and approval odds.

- Down payment size: A larger down payment can strengthen affordability and reduce loan risk.

- Interest rates: Higher rates can shrink what’s comfortable at the same income.

- Loan term and type: Different products come with different payment structures and limits.

Income multiplier vs. what you can comfortably afford

Qualifying and comfortably affording aren’t always the same. Even if a multiplier suggests a certain price point, a realistic budget should also leave room for savings, emergencies, and everyday life. If you want a deeper breakdown of how income multipliers are used and what to consider alongside them, visit https://freshdropsboutique.shop/what-is-an-income-multiplier/.

FAQ

What is the debt-to-income ratio (DTI), and why does it matter for home buying?

DTI compares your monthly debt payments to your gross monthly income. Lenders use it to judge how much room you have to take on a mortgage payment without overextending your budget.

Leave a comment